Be honest: how many "expense tracker" apps have you installed and quietly deleted? If the number is more than one, you're not bad with money — the apps were bad at fitting your life.

India doesn't run on one card and one bank app. You pay rent by NEFT, split dinner on PhonePe, order lunch from a wallet, and swipe HDFC for flights. "Best money app" here doesn't mean the prettiest charts. It means something that sees all of that without you becoming a part-time accountant. That's the bar Mera Kharcha was built for — and why, for a lot of people, it ends up being the only app that stays on the home screen.

The Three Kinds of Money Apps (And Why Most Fail You)

Before we talk about why Mera Kharcha wins, it helps to see what you've probably already tried:

1. The "type every rupee" apps

Clean UI, nice categories, guilt when you forget lunch. By day four you're behind. By day nine you've stopped opening it. Manual tracking works for monks and spreadsheet nerds — not for someone who taps UPI twelve times before lunch.

2. The "link your bank" apps

Account Aggregator sounded great: one login, all accounts. In practice you get OTP fatigue, sessions that expire, banks that sync slowly, and a quiet worry about who holds your credentials. Useful for some — but a lot of users bounce at the permission screen.

3. Your bank's own app

SBI shows SBI. PhonePe shows PhonePe. Neither shows the full picture. You still don't know why salary vanished by the 18th — you only know each app thinks its slice looks fine.

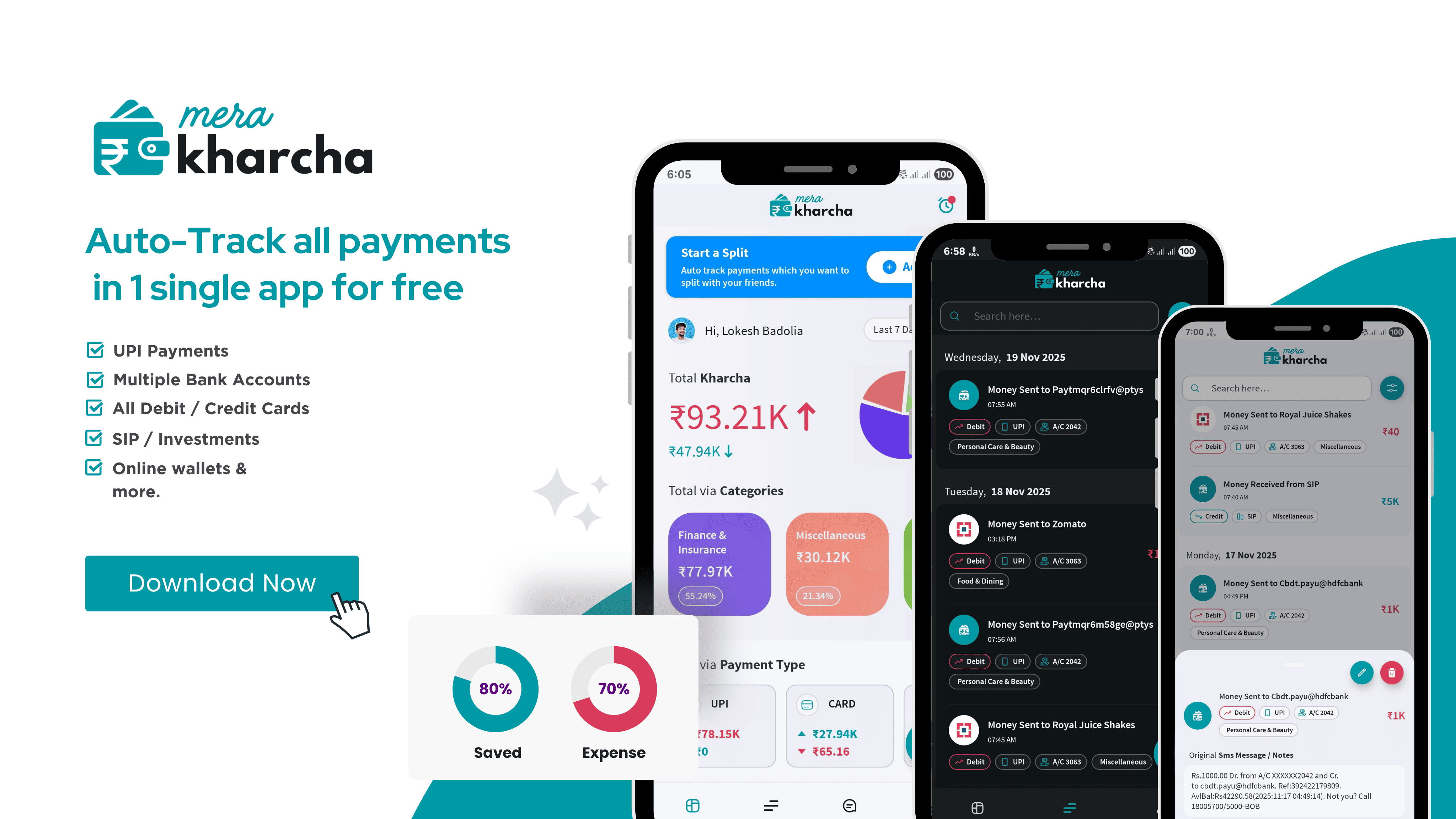

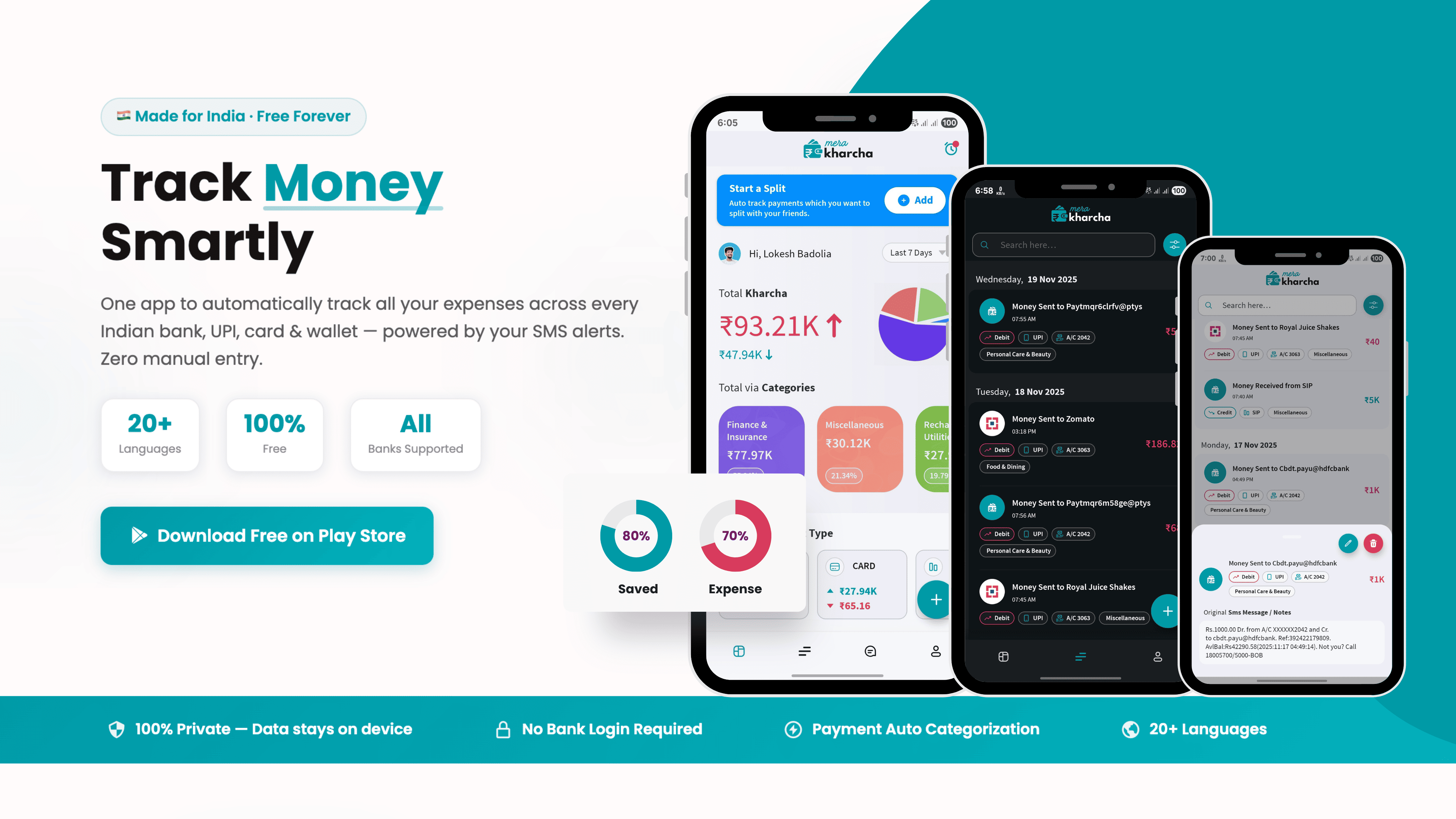

Mera Kharcha sits in a fourth category almost nobody markets well: it uses the paper trail you already get — transaction SMS — and turns that into a full money picture on your phone. No typing. No net banking password. No waiting for a cloud sync.

What "Best" Actually Means for Kharcha in India

Search "best kharcha app" and you'll get lists written for SEO, not for your Tuesday evening. Here's what matters in real life:

- Completeness — UPI + savings + credit card + wallet, not one silo

- Zero daily effort — if it needs discipline, it will lose to Swiggy

- Trust — your data shouldn't live on a stranger's server by default

- Local reality — EMIs, SIPs, family sharing, split trips, Hindi/Gujarati UI

- Actually free to start — not "free" until you need the one feature you downloaded for

Mera Kharcha isn't best because it has the most badges on the Play Store. It's best because it scores high on all five without asking you to change how you pay.

The SMS Trick Everyone Overlooks

Every time money moves, your bank or UPI app texts you: amount, merchant, time, account. That message is already your receipt. Mera Kharcha reads those alerts on your device and builds a running ledger — categorized, searchable, month-wise.

You're not giving the app a new data source. You're finally using the one that's been in your inbox for years. That's why it feels almost unfair compared to apps that make you re-enter what the bank already told you.

Five Reasons Mera Kharcha Beats the Rest — Honestly

1. It wins on completeness without the login drama

HDFC debit, ICICI credit, Paytm wallet, Google Pay, Amazon Pay — if it sends an SMS, it's in one timeline. Competitors either need you to log each payment or pray your bank's API sync works today.

2. Privacy isn't a footer link — it's the architecture

Processing stays on your phone. Your kharcha history isn't uploaded to build someone else's dataset. In 2026, that matters. A lot of users tell us this is the reason they chose Mera Kharcha over "link everything" alternatives.

3. It's built for Indian money chaos, not a US budgeting template

EMI reminders pulled from SMS patterns. Split windows for Goa trips. Family mode so parents and spouse see household spend without sharing passwords. Twenty-plus languages so "kharcha" feels like home, not homework.

4. It survives the "enthusiasm cliff"

The #1 reason finance apps fail isn't missing features — it's abandonment. Mera Kharcha doesn't need a Sunday review ritual. You live normally; the dashboard updates. That's why people who hated tracking suddenly check categories before big purchases.

5. The free tier does the job people actually downloaded for

Automatic tracking, multi-bank SMS support, core categorization — free. Premium adds depth for power users, but you're not held hostage for the basic promise: see where my money went.

How It Compares to What You Might Use Today

Excel or a notebook? Accurate if you're relentless. Most of us aren't. Mera Kharcha is the notebook that writes itself.

Bank + UPI apps only? Fine for checking balance, useless for "why am I broke." Mera Kharcha connects the dots across apps.

Another expense tracker you abandoned? Ask one question: did it track yesterday's chai without you typing it? If not, it was never going to be the best — just the best-looking.

We're not claiming magic. If a payment never generates SMS, it won't appear — same limitation every SMS-based system has. For 95% of daily Indian spending, that's not the bottleneck. Forgetting to log is.

Who Should Switch Today?

If you earn in India, pay digitally, and have ever said "where did my salary go?" — you're the audience. Salaried folks with multiple accounts, freelancers with irregular inflows, couples managing rent + EMIs + parents' medicine — Mera Kharcha is best when your money life is messy and you want clarity without a second job.

Install once. Grant SMS permission. Give it ten minutes to read recent alerts. Then compare your first automatic month summary to whatever you were doing before. Most people don't go back.

Try the App That Stays Installed

The best money app isn't the one with the flashiest launch video. It's the one still on your phone in June — because it never asked you to be perfect, only honest about where the rupees went.

Download Mera Kharcha FreeFrequently Asked Questions

Why is Mera Kharcha better than apps that need bank login?

Bank-login apps depend on third-party sync, OTP cycles, and remote storage. Mera Kharcha uses SMS you already receive — processed locally — so you get broad coverage without handing over net banking credentials.

Is it really the best kharcha app if I only use UPI?

Especially then. UPI volume is high and easy to lose track of. Every PhonePe or GPay debit that texts you is captured automatically, including those ₹49 spends that add up silently.

Will it work with my language?

Mera Kharcha supports Hindi, Gujarati, Marathi, Tamil, Telugu, Kannada, Bengali, and more — important if "best" also means usable for your parents, not just English-first users.

What if I already use another tracker?

Keep it if you love typing. If you don't, run Mera Kharcha parallel for one week. The gap between "what you think you spent" and "what SMS proves you spent" is usually the moment people switch for good.